Your Custom Text Here

Banking on Ideas

Columbia M.Arch 1 – Semester II

Critic: William Arbizu

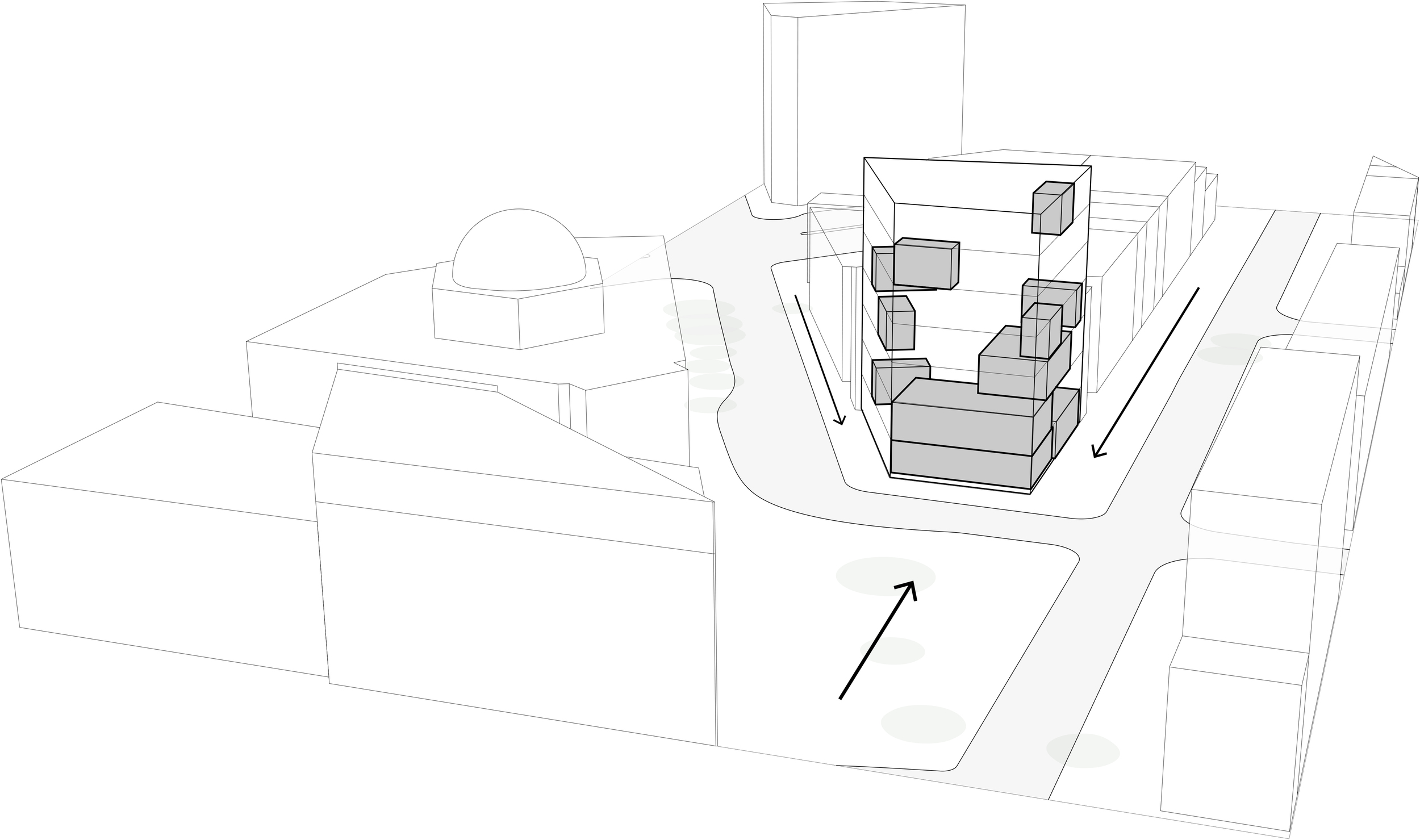

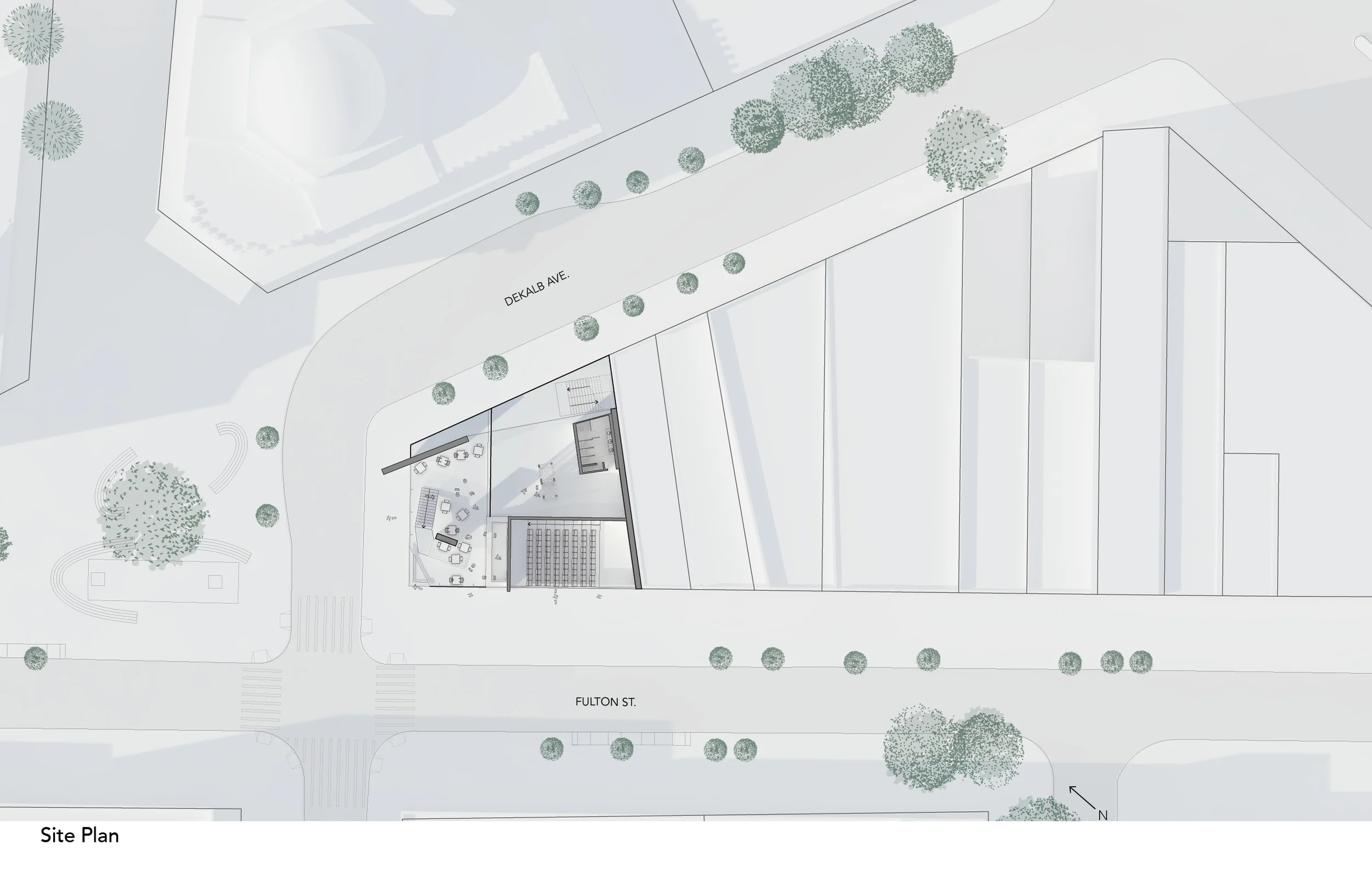

The site is the ideal nucleus for a start up tech company. For employees it is surrounded by new cafes and bars, it is within walking/biking distance from both residential communities (on three sides) and vibrant culture. For employers, the proximity to other tech companies, educational institutions and a young, educated workforce is ideal.

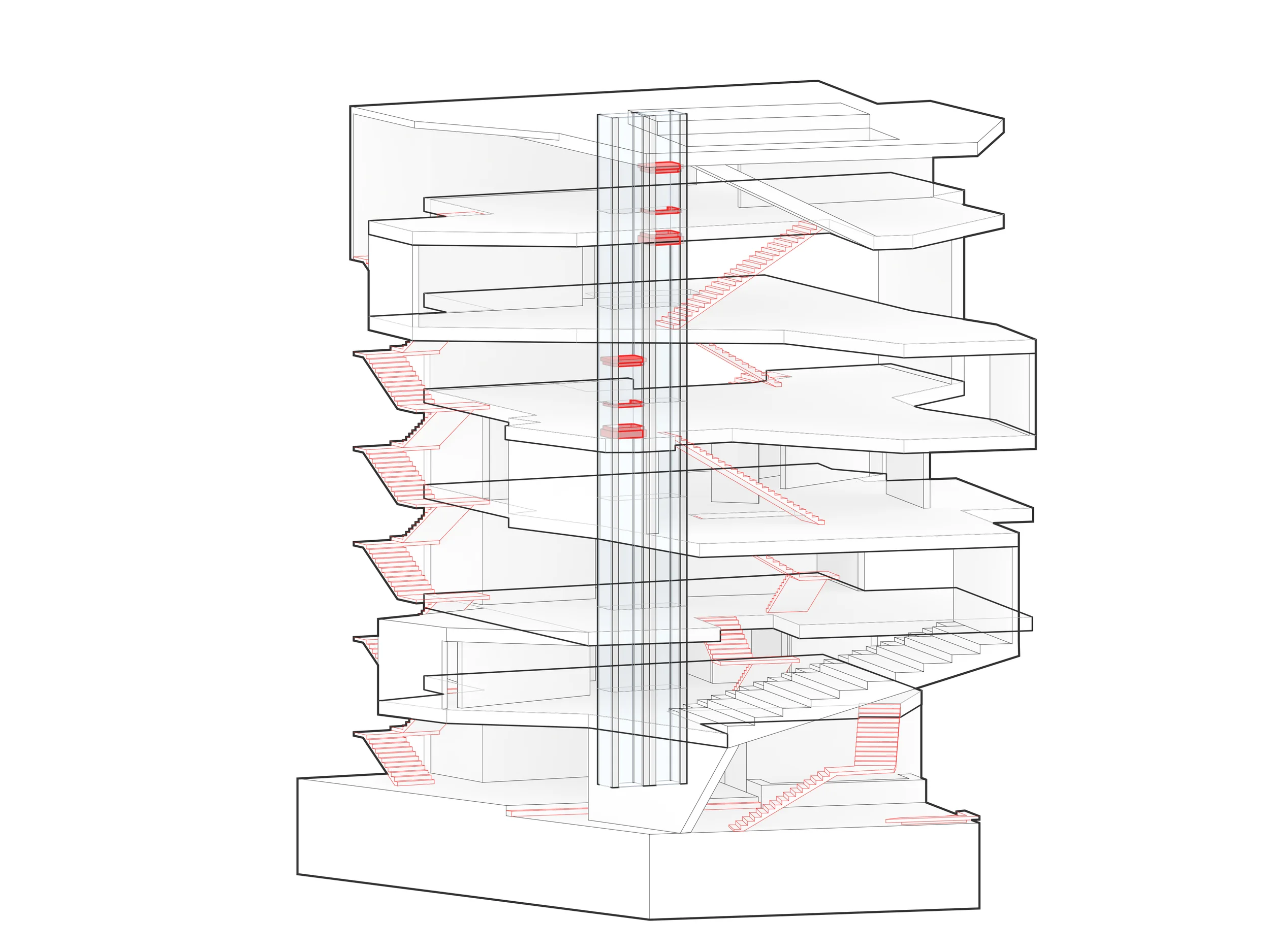

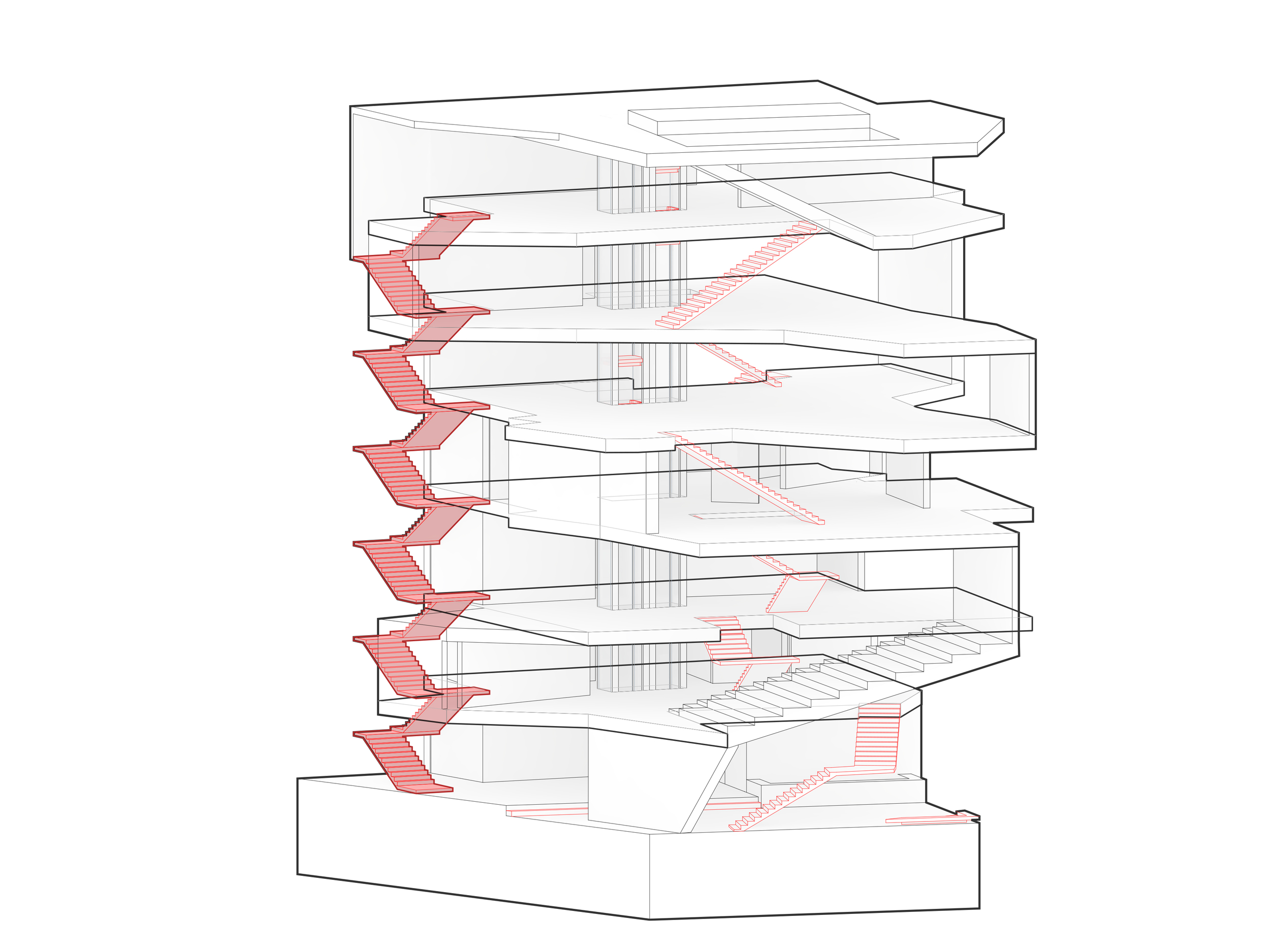

Behind many major start ups are venture capitalists who take a risk and provide support from the get-go. However — particularly after the great recession — access to this network is often unavailable to those just beginning, and from “unconnected” backgrounds. At a time where the conventional bank, as a financial institution, is undergoing dramatic shifts in typology the opportunity to implement one in this community begs the question, “how can a bank contribute productively to a community in a mutually beneficial relationship?”

I believe the bank as a community venture capitalist fills this role. Typically only 44% of startups remain in business. In stark contrast, 87% of firms that have been through an incubator remain in business. Therefore, providing access and continuing support, on a variety of levels, to start-ups profits not only the community but also the bank, and by extension the local community. Small start-ups get access on an unprecedented level to a service previously reserved for an inner circle and the bank has the opportunity not only to help young local entrepreneurs but also a chance to profit off an early investment.

Banking on Ideas

Columbia M.Arch 1 – Semester II

Critic: William Arbizu

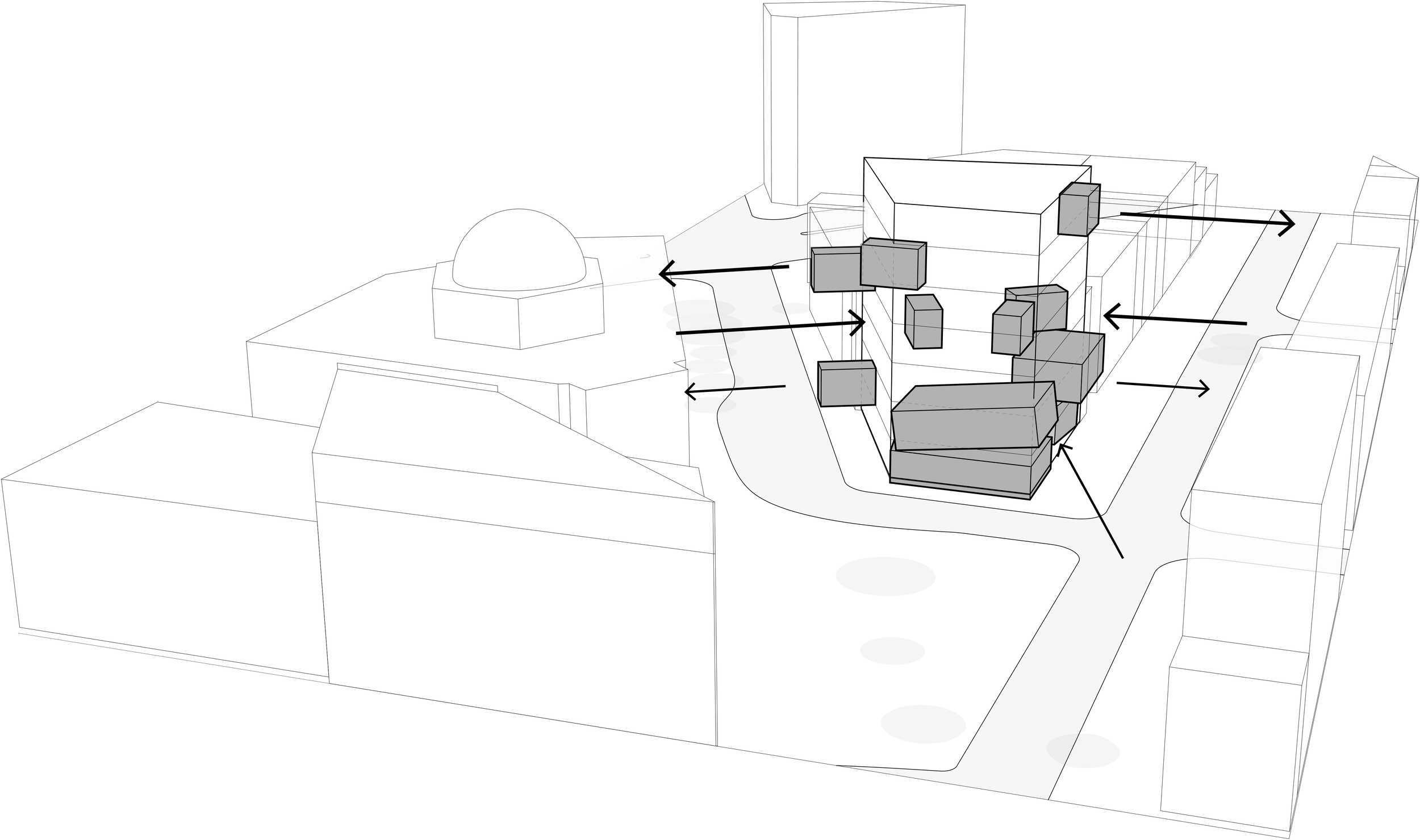

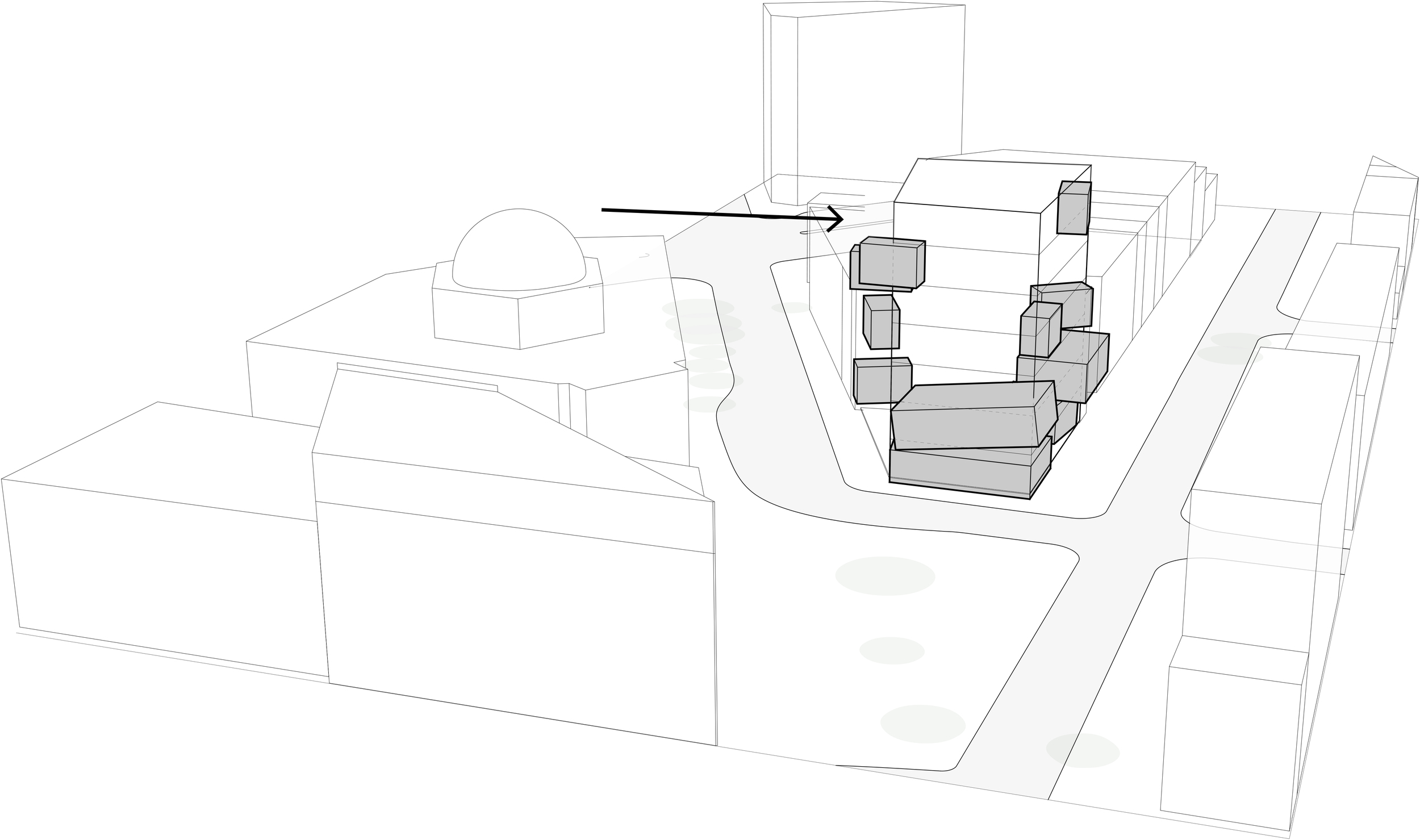

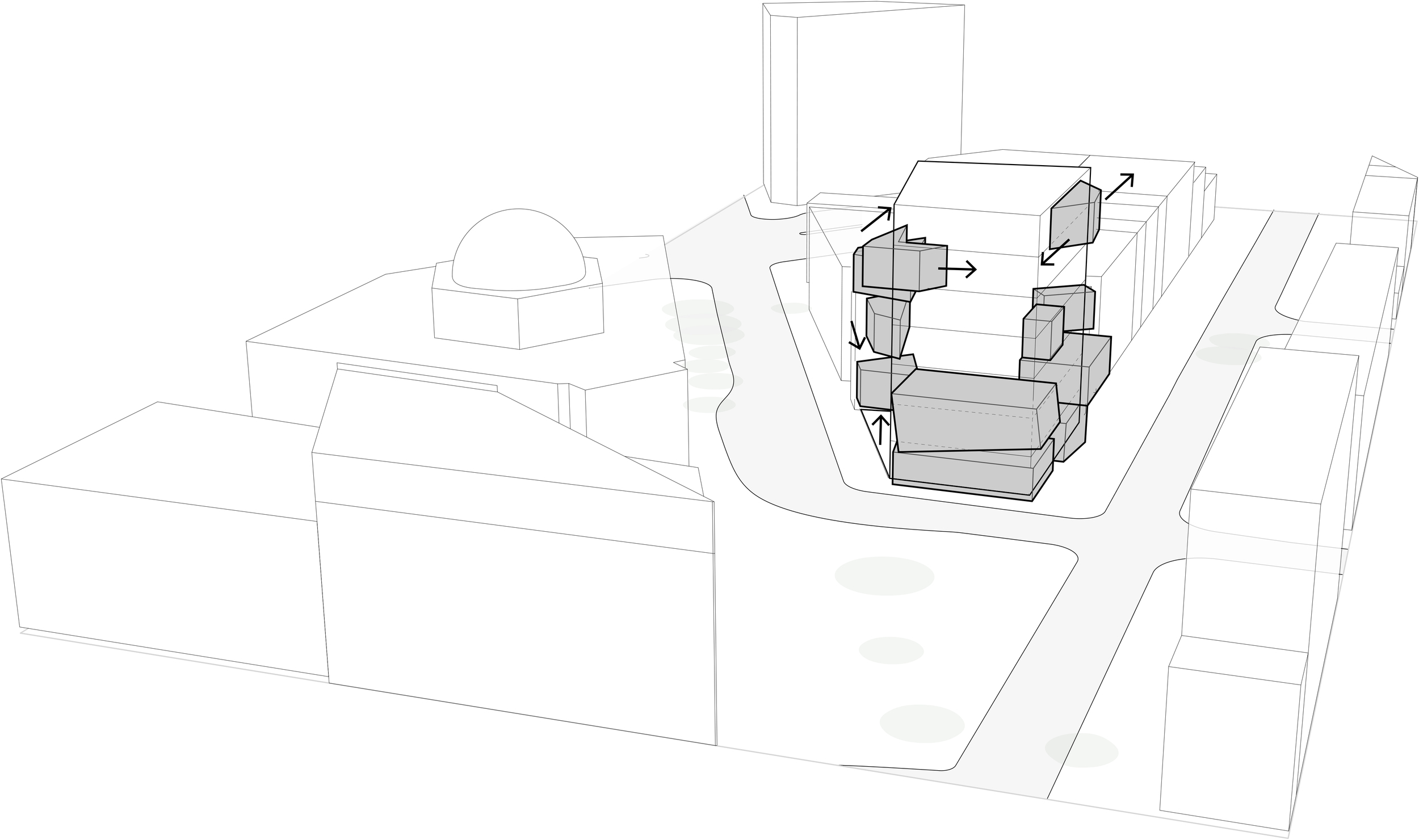

The site is the ideal nucleus for a start up tech company. For employees it is surrounded by new cafes and bars, it is within walking/biking distance from both residential communities (on three sides) and vibrant culture. For employers, the proximity to other tech companies, educational institutions and a young, educated workforce is ideal.

Behind many major start ups are venture capitalists who take a risk and provide support from the get-go. However — particularly after the great recession — access to this network is often unavailable to those just beginning, and from “unconnected” backgrounds. At a time where the conventional bank, as a financial institution, is undergoing dramatic shifts in typology the opportunity to implement one in this community begs the question, “how can a bank contribute productively to a community in a mutually beneficial relationship?”

I believe the bank as a community venture capitalist fills this role. Typically only 44% of startups remain in business. In stark contrast, 87% of firms that have been through an incubator remain in business. Therefore, providing access and continuing support, on a variety of levels, to start-ups profits not only the community but also the bank, and by extension the local community. Small start-ups get access on an unprecedented level to a service previously reserved for an inner circle and the bank has the opportunity not only to help young local entrepreneurs but also a chance to profit off an early investment.